Why legacy KYC fails in 2026

Traditional Know Your Customer (KYC) frameworks rely on siloed databases and static, rule-based checks. These linear systems treat customer data as isolated points, failing to capture the interconnected nature of modern financial crime. In 2026, illicit networks operate as complex, decentralized graphs, utilizing layered shell companies, cross-border transactions, and synthetic identities to obscure beneficial ownership. Legacy tools cannot trace these non-linear relationships, leaving institutions blind to sophisticated money laundering schemes.

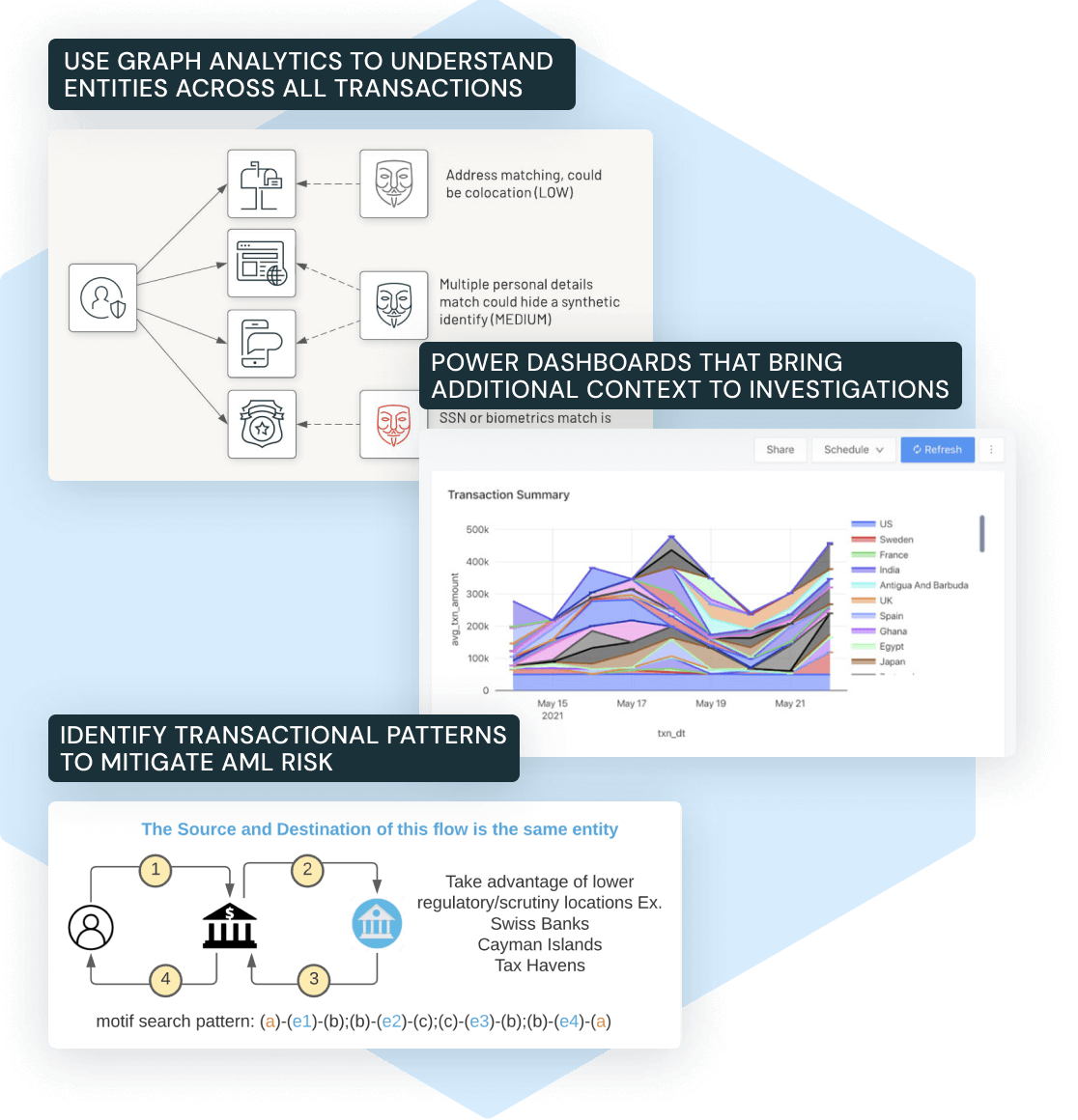

Graph technology restructures verification by mapping relationships rather than just profiles. In a KYC graph, individuals and entities are nodes, while financial transactions, shared addresses, or directorships are edges. This structure allows compliance teams to detect hidden associations instantly. For example, a single node might appear low-risk in isolation, but when connected to multiple sanctioned entities through indirect edges, the risk profile changes dramatically. This visual and computational clarity is impossible with traditional relational databases.

The cost of this technological lag is measurable and growing. Regulatory bodies continue to emphasize the need for holistic risk assessments. Institutions relying on outdated checks face rising false positives, operational bottlenecks, and severe regulatory fines. The inability to adapt to real-time network analysis is no longer just an efficiency issue; it is a compliance vulnerability.

Mapping connections with the KYC Graph

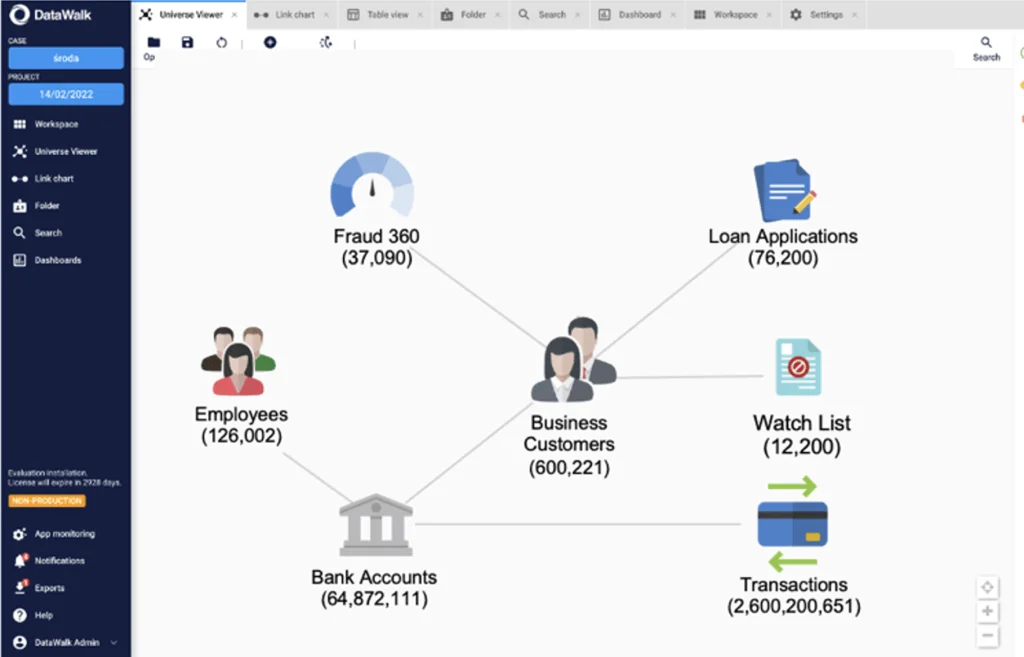

Traditional compliance systems often treat customer data as isolated records, making it difficult to detect complex financial crime networks. A KYC graph database solves this by unifying disparate data sources into a single, interconnected model. In this architecture, entities such as individuals, companies, and bank accounts are represented as nodes, while the relationships between them—such as ownership, employment, or transaction history—are represented as edges. This structure allows institutions to map the full ecosystem of a client rather than viewing them in silos.

The primary advantage of this approach is the ability to reveal hidden ownership structures and indirect control. By traversing multiple degrees of separation, compliance teams can identify ultimate beneficial owners (UBOs) who might otherwise remain obscured through layers of shell companies. For example, if a high-risk individual owns 5% of Company A, which in turn owns 10% of Company B, a graph query can instantly surface the entire chain. This capability is essential for meeting stringent requirements regarding beneficial ownership transparency, as outlined by global regulatory standards.

This unified view significantly reduces false positives in anti-money laundering (AML) screening. Instead of flagging every transaction involving a high-risk jurisdiction, the graph context helps distinguish between benign and suspicious activity by analyzing the broader network behavior. As regulatory expectations evolve, particularly with updates from the U.S. Securities and Exchange Commission (SEC) and central banks, the ability to provide real-time, auditable evidence of these relationships becomes a critical component of modern compliance infrastructure.

Detecting hidden ownership and sanctions

Traditional compliance checks often stop at the first layer of corporate structures, leaving beneficial owners obscured behind shell companies. Graph analytics resolve this opacity by mapping the entire network of relationships. Instead of evaluating entities in isolation, the system treats every individual, company, and trust as a node connected by specific edges, such as voting rights, directorships, or shared addresses.

This structure allows compliance teams to trace influence through multiple layers of ownership. For example, a node representing a holding company might connect to three subsidiary nodes, each linked to a final beneficial owner. By following these edges, systems can identify indirect control that manual reviews frequently miss. As noted in recent legal-entity knowledge graph frameworks, every fact in the graph must include a source and timestamp to ensure auditability and version control (OpenCorporates, 2025).

Matching entities against dynamic sanctions lists requires real-time verification. When a new connection is discovered in the graph, the system immediately cross-references it against updated regulatory lists from bodies like the FATF and the SEC. This continuous monitoring ensures that compliance status reflects current risks rather than historical snapshots. The combination of graph analytics and machine learning enables organizations to address these complex KYC challenges more effectively while meeting strict regulatory obligations (DataWalk, 2025).

-

Verify beneficial ownership layers beyond the primary entity

-

Check for shared directors or addresses across unrelated nodes

-

Cross-reference all connected entities against current sanctions lists

-

Ensure every data point includes a source and timestamp for audit trails

Automating Investigations with AI Agents

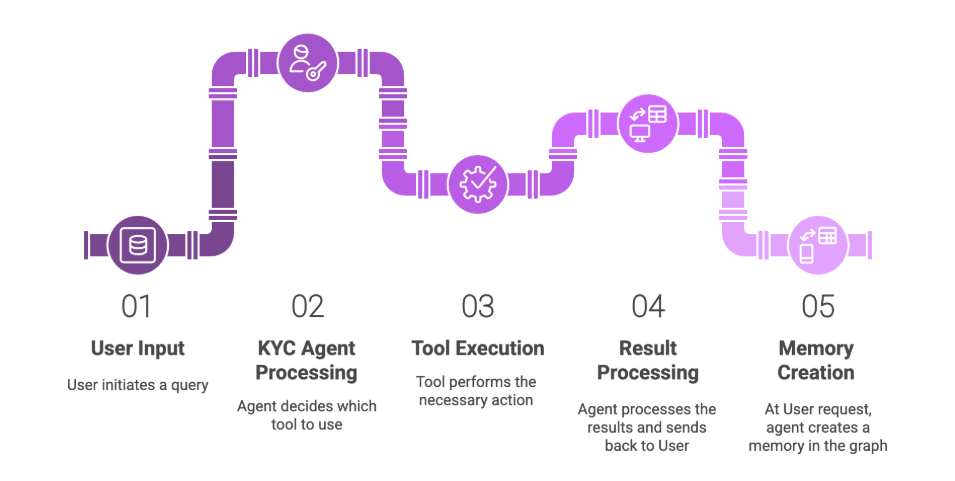

The integration of GraphRAG (Retrieval-Augmented Generation) and autonomous AI agents represents a significant shift in fraud detection workflows. Rather than relying on static rule sets, these systems leverage graph structures to map complex relationships between entities. In this context, nodes represent actors—such as individuals, corporate entities, or bank accounts—while edges denote the transactions or ownership links connecting them. This architecture allows AI agents to traverse these networks in real time, identifying subtle anomalies that traditional keyword-based searches might miss.

By equipping KYC agents with frameworks like OpenAI’s Agents SDK and tools like MCP, institutions can automate the initial stages of investigation. An AI agent can query a graph database to uncover hidden connections, such as shared addresses or indirect ownership ties, and then synthesize these findings into a coherent narrative. This reduces the manual burden on compliance analysts, allowing them to focus on high-risk cases that require human judgment rather than routine data gathering.

The goal is not to replace human oversight but to augment it with graph-native intelligence. As noted by industry providers like Prescott Data, this approach maps criminal networks and resolves entity identity across institutional boundaries without requiring the sharing of sensitive raw data. This preserves privacy while enhancing the depth of due diligence. The trend aligns with broader regulatory expectations for more dynamic, risk-based approaches to financial crime prevention, moving beyond static checklists toward continuous, intelligent monitoring.

Timeline of KYC graph adoption

The integration of graph databases into compliance workflows has shifted from isolated data silos to real-time, interconnected identity verification systems. This evolution reflects the increasing complexity of financial crime networks, where traditional relational databases struggle to map hidden relationships between nodes and edges.

Financial institutions began testing graph technology to uncover hidden ownership structures. These early implementations focused on mapping complex corporate hierarchies, allowing investigators to identify ultimate beneficial owners (UBOs) through direct node traversal rather than rigid table joins.

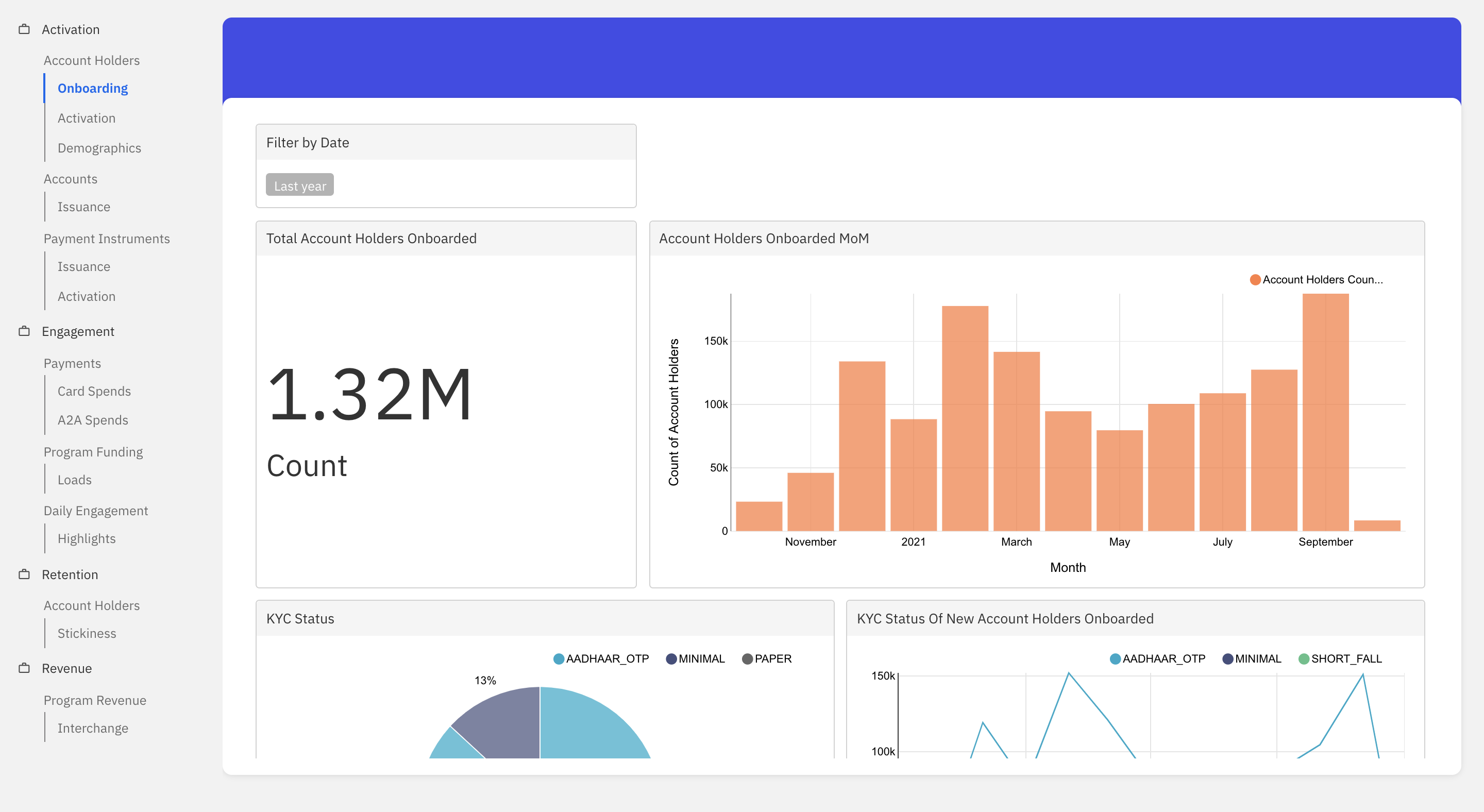

Following major regulatory fines, banks scaled graph solutions to handle larger datasets. The focus shifted to reducing false positives in anti-money laundering (AML) alerts by contextualizing transactions within a broader network of customer relationships, a capability highlighted by industry analyses of graph database utility in banking.

KYC graph adoption matured into real-time decisioning engines. Instead of periodic batch updates, systems now evaluate identity risks instantly during onboarding. This shift allows institutions to detect synthetic identities and ring fraud by analyzing edge weights and connection patterns in milliseconds.

Current standards combine graph traversal with machine learning models to predict emerging financial crime trends. These systems continuously learn from new regulatory guidance and transaction data, automatically adjusting risk scores based on the evolving topology of customer networks.

Frequently asked questions about KYC Graph

How does graph analytics improve identity verification compared to traditional methods?

Graph analytics transforms isolated data points into a connected network, allowing institutions to visualize relationships between entities. By mapping nodes (individuals, companies, accounts) and edges (transactions, shared addresses), systems can detect complex fraud rings that rule-based systems miss. This approach aligns with recommendations from the Financial Action Task Force (FATF) for using technology to enhance customer due diligence and mitigate money laundering risks.

Is graph-based KYC compliant with current regulations?

Regulatory bodies, including the SEC and various central banks, are increasingly recognizing graph analytics as a valid tool for regulatory compliance. The key is ensuring data lineage is preserved. As noted by OpenCorporates, every fact in a legal-entity knowledge graph must include the source and timestamp to maintain auditability. This ensures that the graph structure supports transparent, defensible decision-making required by anti-money laundering (AML) frameworks.

What are the privacy implications of using graph structures?

Graph analytics processes personal data to identify patterns, requiring strict adherence to data protection laws like GDPR. Institutions must implement privacy-by-design principles, ensuring that node and edge data are anonymized or pseudonymized where possible. The focus is on analyzing relationships rather than storing excessive personal details, thereby minimizing privacy risks while maintaining the integrity of the identity verification process.

No comments yet. Be the first to share your thoughts!