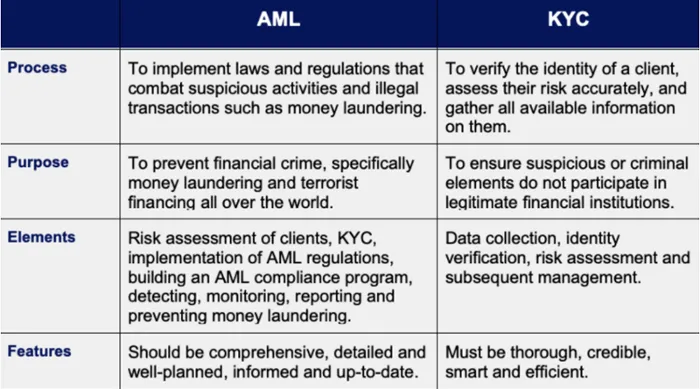

KYC vs AML 2026: Core Differences

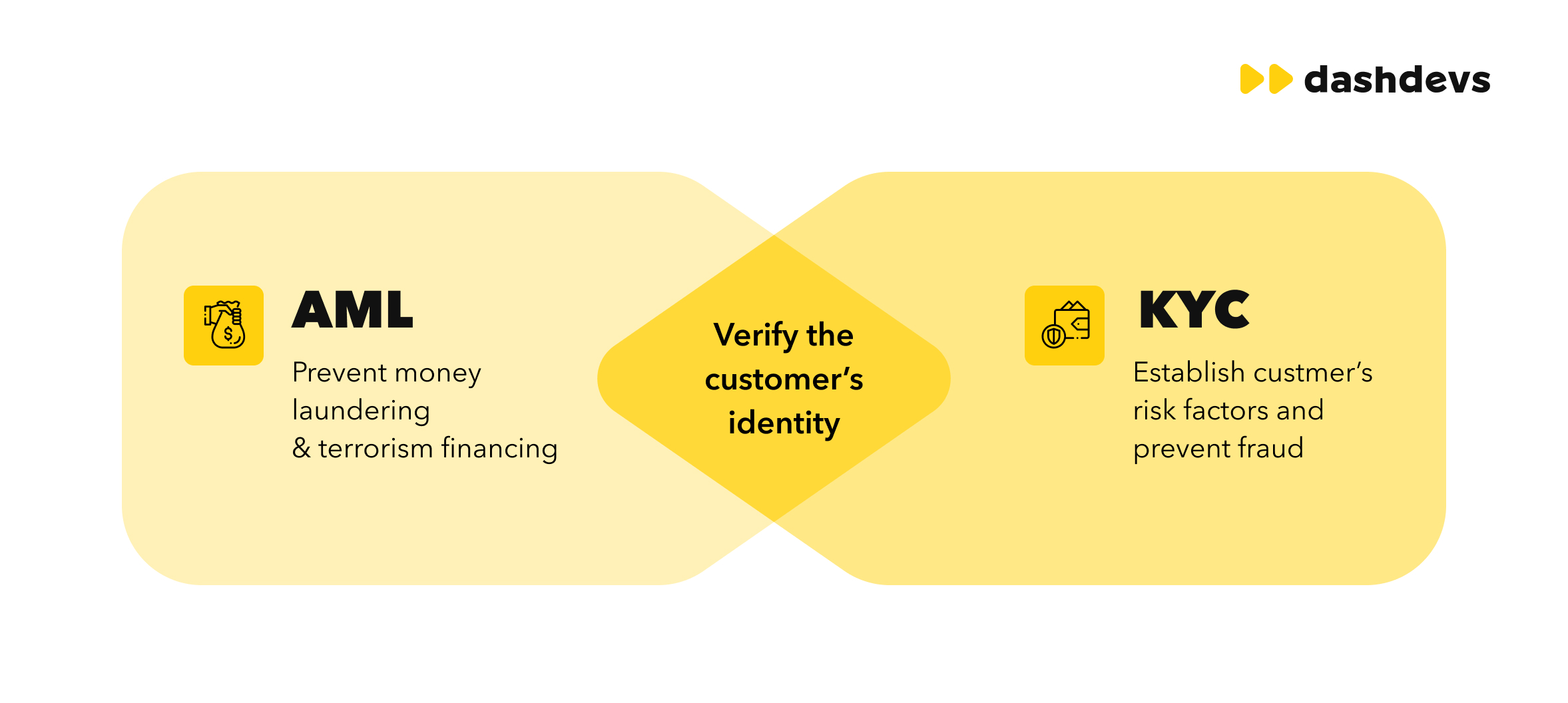

KYC and AML are often grouped together, but they serve distinct functions in the compliance lifecycle. Know Your Customer (KYC) is the entry-point identity layer. It verifies who a customer is during onboarding. Anti-Money Laundering (AML) is the continuous compliance infrastructure built on top of that foundation. A program can have strong KYC and still fail AML if it lacks ongoing monitoring.

In 2026, the gap between these two functions is widening. KYC has shifted from static document checks to dynamic, AI-driven identity verification. AML has evolved from policy-driven frameworks to practical, risk-based implementation. Regulators are no longer focused solely on whether controls exist; they expect firms to demonstrate that those controls work effectively in real-world scenarios.

The core difference lies in timing and scope. KYC is a point-in-time event, albeit one that requires periodic updates. AML is a continuous process that tracks transactions and behavior over time. Think of KYC as the gatekeeper at the door and AML as the security team monitoring the building.

This distinction matters because the 2026 landscape demands more than just accurate onboarding. It requires seamless integration between identity verification and transaction monitoring. AI is the bridge that connects these two domains, enabling firms to verify identities instantly while simultaneously assessing risk in real time.

KYC vs AML 2026 comparison

KYC and AML are compliance requirements that work differently. KYC is the entry-point identity layer; AML is the continuous compliance infrastructure built on top. A program can have strong KYC and still fail AML checks if ongoing monitoring is weak.

In 2026, regulators are no longer focused solely on whether controls exist. They expect firms to demonstrate that those controls work effectively in real-world scenarios. This shift means KYC and AML must be integrated, not siloed.

| Dimension | KYC | AML |

|---|---|---|

| Timing | At onboarding and periodic reviews | Continuous throughout the relationship |

| Scope | Identity verification and due diligence | Transaction monitoring and risk assessment |

| Technology | AI-powered identity verification | AI-driven anomaly detection |

| Regulatory Focus | ||

| Primary Goal | Confirm who the customer is | Detect suspicious activity |

2026 Regulatory Shifts and AI Oversight

The regulatory landscape for KYC vs AML 2026 is undergoing a fundamental restructuring. Regulators are moving beyond checking boxes to demanding demonstrable effectiveness. Under frameworks like the EU AI Act, systems used in anti-money laundering (AML) and KYC are classified as high-risk. This classification brings new, stringent obligations regarding transparency, data governance, and human oversight.

Explainable AI is Now Mandatory

In 2026, black-box algorithms are no longer acceptable for compliance decisions. The EU AI Act requires that high-risk AI systems provide sufficient transparency to enable human review. This means your KYC and AML tools must be able to explain why a transaction was flagged or a customer rejected. If an AI model cannot provide a clear, auditable reason for its decision, it fails the regulatory test.

This shift impacts the core difference between KYC and AML 2026. While KYC focuses on identity verification at onboarding, AML requires continuous, explainable monitoring. Regulators expect firms to prove that their controls work in real-world scenarios, not just on paper. The burden of proof has shifted from "we have a system" to "our system is understandable and accountable."

Practical Risk-Based Implementation

Compliance teams must now demonstrate that their AI-driven controls are effective. This requires a shift from policy-driven frameworks to practical, risk-based implementation. You must be able to show that your AI models are regularly tested, validated, and aligned with current threat landscapes. Failure to do so exposes firms to significant regulatory penalties and reputational damage.

The key takeaway for KYC vs AML 2026 is that AI is no longer just a tool for efficiency; it is a regulated asset. Your compliance strategy must prioritize explainability and human oversight to meet these new standards. Ignoring these requirements is no longer an option.

| Aspect | Traditional Approach | 2026 Requirement |

|---|---|---|

| AI Decisioning | Black-box automation | Explainable, auditable outputs |

| Compliance Focus | Policy existence | Demonstrable effectiveness |

| Regulatory Status | Low risk | High-risk (EU AI Act) |

AI Identity Verification in Practice

By 2026, the distinction between KYC and AML is no longer defined by separate tools, but by how artificial intelligence processes identity and behavior data. The industry has shifted from static, manual reviews to intelligent, continuous monitoring. This transition requires systems that can verify who a customer is at onboarding and simultaneously monitor their financial activity for anomalies in real time.

KYC: Biometric and Document Verification

In the KYC space, AI has replaced manual document checks with automated, high-accuracy verification. Systems now use computer vision to analyze identity documents for signs of forgery, such as altered holograms or inconsistent fonts. More importantly, they integrate liveness detection and facial recognition to ensure the person presenting the ID is physically present and matches the photo.

This approach reduces friction for legitimate users while blocking synthetic identity fraud, which has become increasingly sophisticated. Instead of a one-time check, some platforms are moving toward "continuous KYC," where identity is re-verified periodically or triggered by risky behavior changes. This ensures that the customer remains who they claim to be throughout their entire relationship with the firm.

AML: Transaction Monitoring and Graph Analytics

AML compliance has evolved from rule-based transaction monitoring to predictive analytics. Traditional systems often generated excessive false positives, forcing compliance teams to manually review benign activity. AI models now analyze transaction patterns against global behavioral baselines, flagging only truly suspicious events.

Graph analytics plays a critical role here. By mapping relationships between accounts, entities, and geographies, AI can detect complex money laundering networks that simple rule-based filters miss. This allows firms to identify sanctions evasion and terrorist financing rings more effectively. As noted by industry observers, the focus is shifting from merely having controls in place to demonstrating that those controls work effectively in real-world scenarios.

Choosing the Right Compliance Approach

Integrating KYC and AML systems effectively requires moving away from siloed workflows. As enforcement expectations rise in 2026, regulators expect firms to demonstrate that controls work effectively in real-world scenarios, not just that they exist on paper [src-serp-4]. A unified platform ensures that identity verification feeds directly into transaction monitoring, preventing fragmented risk assessments.

1. Map Regulatory Expectations for 2026

Begin by auditing your current controls against the shift toward risk-based implementation. The focus is no longer solely on policy existence but on practical effectiveness. Identify gaps where KYC data is not automatically triggering AML alerts, creating blind spots in your compliance framework.

2. Evaluate Platform Integration Capabilities

Choose a solution that unifies customer onboarding with ongoing monitoring. Siloed systems separate AML from KYC and payment workflows, leading to redundant checks and delayed risk detection. A single platform reduces latency and ensures that identity changes are immediately reflected in transaction risk scores.

3. Assess Resource Constraints and Scalability

Credit unions and community lenders face the same KYC and AML requirements as large banks, but with fundamentally different resources [src-serp-6]. Select a system that scales with your transaction volume without requiring disproportionate manual intervention. Automated identity verification should handle the bulk of initial screening, allowing your team to focus on high-risk exceptions.

4. Implement Continuous Monitoring

KYC is not a one-time event. Ensure your chosen approach includes continuous monitoring that updates customer risk profiles based on new transaction data or adverse media. This proactive stance aligns with the 2026 trend of demonstrating active, effective compliance rather than static adherence to checklists.

Frequently asked: what to check next

[1] https://www.lseg.com/en/risk-intelligence/glossary/aml/aml-kyc [2] https://namescan.io/insights/aml-compliance-trends-2026/

No comments yet. Be the first to share your thoughts!